.jpg)

The toxic brew of fiscal populism, crony capitalism and bad economic management has ensured the collapse of economic growth, industrial stagnation, stubbornly high consumer inflation, declining savings and investment, shrinking employment opportunities, and a dangerously vulnerable external financing situation.

If the Greek crisis spirals into a larger European sovereign debt crisis and possible fragmentation of the eurozone, India's trade and capital flows could be hit, says Shankar Acharya.

Only a mix of sterilised currency intervention and capital account management can halt the rupee's rise, says Shankar Acharya.

The expenditure cuts are one-off, too much has been given away in tax cuts and there are few green shoots of reform.

The most important thing for India is to resurrect public health services in the country, says Shankar Acharya.

Indeed, although total industrial employment grew by over 6 per cent annually, organised industrial sector employment fell by 1 per cent per year, bringing the share of organised industrial sector employment down from 18 per cent (of total industrial employment) in 1998 to only 10 per cent in 2004.

Looking back 20 years from now, the month just gone by will loom even larger in history books.

For those, like me, who backed the Reddy-Mohan approaches to monetary and regulatory policies, the continuity shown by Subbarao's RBI is very heartening. For earlier critics of these approaches there may be some disappointment and discomfort.

The Direct Taxes Code suffers from serious weaknesses.

The simple truth is that BRICs are still too small to be global locomotors unless they sustain double digit growth, which they manifestly can't in the present environment. Of course, the fact that the Asian BRICs are still expected to enjoy moderate growth in 2009, is itself testimony to their resilience in the face of global recession.

The indicators of slowing growth proliferate in the daily papers. The government and RBI are in a small minority in expecting growth in 2008/9 to attain 8.5 to 9 per cent. The great majority of independent analysts expect the outcome to be in the 7 to 8 per cent range, with a growing number favoring the lower side of this band. Equity markets have tanked and stock prices are in doldrums. The really nasty surprise has come from inflation.

What is becoming increasingly clear is that they are an opaque and hugely inadequate response to the current problem of sustained increases (over the last five years) in global oil prices.

Almost every serious government report on tax reforms owes some debt to Amaresh-da.

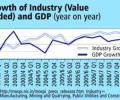

The case for a swift and sizable reduction in the repo rate rests on several pillars. First, and most importantly, there is mounting evidence that the five-year old surge in India's economic growth, especially industrial growth, peaked a few months back.

Has there been a resurgence of the manufacturing sector in India? Shankar Acharya has his doubts.

The Mystery Report lists 48 (!) "Recommended Actions" (mostly in the next two years) for paving the way for Mumbai's rise as an IFC. It's a wide-ranging and challenging list.

If we don't take the fiscal deficit seriously, then it could easily widen and harm our future growth